We’ve seen two big pieces of financial news hugging the headlines recently:

1) The NASDAQ is in correction.

2) The recent inflation trend is more than likely here to stay.

And if you’re a startup founder, you might be starting to sweat.

Why?

Since the NASDAQ holds the majority of the companies, it being “in correction” (AKA down more than 10% since last fall’s high), a lot of the large, publicly-traded tech companies and the IPOs we’ve helped people through over the last few years have seen their stock values plummet.

Also, since the Federal Reserve announced they no longer think the inflation trend is temporary, they’re going to do some things about it… including putting an end to quantitative easing.

Sidebar: What does it mean to end quantitative easing?

Quantitative easing isn’t something that’s gotten a lot of attention since the 2008 financial crisis, but ever since then, the federal reserve has been printing more money.

With the new dollars they print, they buy treasury bonds, treasury bills, and mortgage-backed securities from banks to lower interest rates… the idea was to flood the banks with new cash, making money so available that the banks would have to lend it out at low interest rates. (Here’s a YouTube video that explains it really well.)

With this happening, there’s an interesting threat that the Federal Reserve shrinking its balance sheet (by not buying the new bonds or assets they’ve been in the habit of in the past) poses to venture capital… and by extension, startups and IPOs. (If you have a subscription to The Information, this article is an incredible, well-thought-out analysis of the situation I’d recommend to anyone to read.)

What startup founders need to do with their liquidity… and why a balanced investing portfolio is so, so crucial.

So… what does all this mean if you’re a founder who’s ready to take some liquidity in one of your later-stage investment rounds?

What do you need to do given the state of the NASDAQ and the economy as a whole?

Before we get into the nitty-gritty, I think it’s helpful to zoom out and take a big-picture view of solid financial investing strategies for founders.

With KB Financial Advisors, we built a financial philosophy specifically around the needs of tech founders and tech employees. As a group, you have different interests, needs, and opportunities than people in other lines of work without stock option compensation… which means you need a different approach to financial planning than everyone else, too.

Because of the unique opportunities in your particular world of work, we focus on five key areas that affect your financial plan:

- Career

- Stock options or equity

- Taxes

- Cash flow

- Investments

You can even group these five aspects into three areas:

- Future wealth

- Necessary expenses

- Current wealth

Your future wealth is your career, your equity, and your shares in your company.

Necessary expenses include taxes and living expenses… things everyone has and no one can get away from.

Current wealth is the real dollars in your bank account. (You’ve sold your options, paid your taxes, and now have cash to work with in your investing plan.)

Usually, when founders “cash out” on some of their shares during later-stage funding rounds, they’ll use the money to do one of three things:

- Invest in other tech companies or venture capital funds.

- Purchasing real estate, whether as a family home or investment property.

- Fund their investment portfolio.

As a founder, the purpose of your investment portfolio isn’t just to grow a cushion of cash. It’s to replace your income, fund your living expenses, and support other pieces of your balance sheet. (Like if you wanted to tap your portfolio to purchase real estate or invest in another company, for example.)

Your career & your investments should not be in the same sectors.

I know hearing that can feel like a bucket of ice water to the face, especially to people who love tech so much, but hear me out:

In a perfect world, your career as a founder and your investment portfolio are a good match. Meaning, the risks and threats you face as a founder are matched by the strengths and the opportunities within your investment portfolio.

Unfortunately, this isn’t what we usually see.

(What we often see, instead, is a person’s career and equity is in tech, then they pay their taxes, and the cashflow goes to more tech companies and venture capital for tech companies… so your investment portfolio is also in tech.)

Tech is great, don’t get me wrong, but only having tech throughout your investment portfolio isn’t the most optimal, or balanced thing to do.

Reason #1: Stock market history repeats itself.

So… why don’t you want your entire financial plan to be made up of tech investments?

Let’s circle back to those two big news stories I mentioned at the top of the post:

The NASDAQ is in correction.

On top of that, tech is the single largest sector in the US stock market right now. If you look back over the last five years, it’s gained a bigger piece of the pie every year.

With this in mind, take a step back and think about when you first started your company. More than likely, your goal was to take a “small” idea and create a “big” company around it. When you were granted founders shares, they were probably worth $0.01 or less, meaning you took something that was worth almost nothing, and have created something of real, substantial value.

The reason I point this out is because as a founder, you weren’t banking on something that was already really huge and popular to become even bigger… you were banking on something tiny and miniscule to gain traction and become successful.

Breaking it down: Top 10 Companies by Market Weight

Moving on from tech as a sector, let’s look at the top 10 companies in the US stock market as a whole, and how that’s changed over time. Here’s a really cool animation to see how this has changed from 1995 to 2020. (Seriously: take a few minutes to watch it. No sound needed.)

When you go back to the 1990s, tech didn’t even register in the top 10 US stocks. In the late 90s and early 2000s, Microsoft and Intel came on the scene. In 2000 and 2001, you can see the tech bubble grow, burst, and collapse.

Then, after the mid-2000s (especially after the 2008 financial crisis), the top five companies are all tech.

However, one thing you’ll learn by watching this animation (and that you can see repeated throughout the history of the market in general), is that big does not get bigger. The top companies do get replaced.

We don’t know how or when, but I feel confident saying the companies at the top probably won’t stay there, and that the real growth opportunities for your investment portfolio are in other areas.

Reason #2: You need lower correlation between your career and your investments

At a high level, the definition of correlation is the comparison of the movement of two objects over time. With investment planning, we usually compare the returns of two different assets, whether they’re ETFs, mutual funds, or something else.

A correlation of 1.0 means the two items are perfectly synchronized and move together, like ice skaters in the Olympics. Their movements mirror each other, and they’re perfectly synchronized.

In investing, however, the goal with diversification is to lower correlation. We don’t want everything in your portfolio to be going down at the same time. (Like tech stocks in NASDAQ at the moment.)

But beyond just the stocks you invest in, your career needs a low correlation to your investment portfolio to diversify your financial plan.

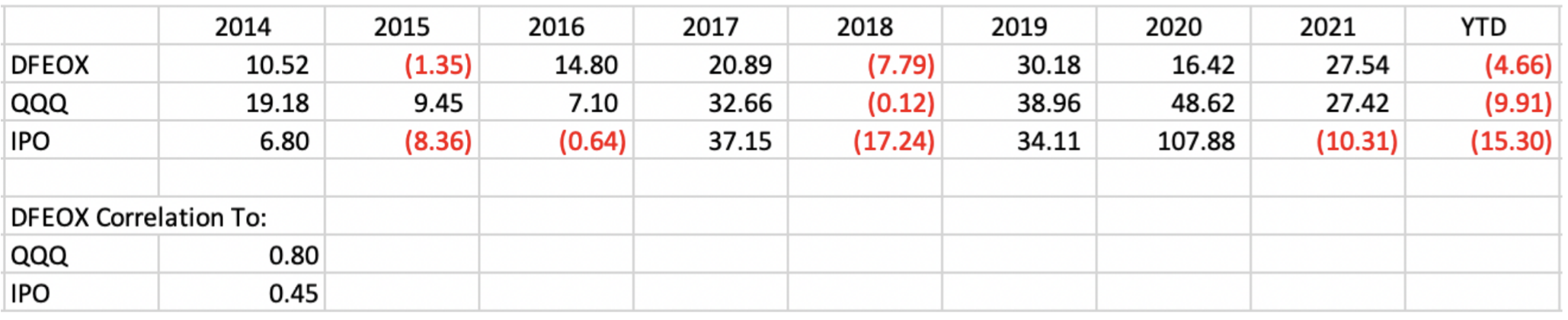

Dimensional US Core 1 vs Nasdaq 100 vs Renaissance IPO ETF

To show you a helpful example of correlation, let’s compare three different mutual funds and ETFs:

- The Dimensional US Core 1 Equity Mutual Fund

- The NASDAQ 100 ETF

- The Renaissance IPO ETF

???? I’ll talk more about funds offered by Dimensional Fund Advisors in a few paragraphs, and I think you’ll really like them… stay tuned. ????

- The Dimensional US Core 1 Equity Mutual Fund (DFEOX)

This is one of three core US stock funds Dimensional offers that represent the entire US stock market. (They have Core 1, Core 2, and Vector.) I chose Core 1 for the example, because we use it with a lot of our clients, and it tilts towards small cap and value.

It’s got 2,491 different stocks.

- The NASDAQ 100 ETF (QQQ)

When you look at the top 10 holdings of QQQ, it’s the big tech companies: Facebook, Google, Microsoft, Amazon, etc.

It’s more or less the big tech ETF, with 102 individual stocks.

- The Renaissance IPO ETF (IPO)

I track this one every day, because it’s the closest representation of the companies our clients work for. Our clients are pretty evenly divided between pre-IPO and post-IPO companies, and almost all of the people in the post-IPO group have their companies included in the ETF. This gives me a picture of the bigger trend of how our clients’ companies are doing in the market.

Here’s a chart comparing the correlation of all three of these since 2014:

As you can see, the Core 1 fund is closely correlated to big tech (QQQ). It doesn’t exactly mirror the movements of big tech, but it’s really close because so much of the total stock market index is made up of big tech. (If you wanted lower correlation to QQQ, you could choose Dimensional Fund Advisors’ Core 2 or Vector funds instead.)

The IPO fund, on the other hand, isn’t very correlated with Core 1. This is what we want. Your investment portfolio needs to act differently than the equity you still hold in your company.

Looking at the chart, you can also see how DFEOX lags behind QQQ until 2021 and 2022 YTD. From 2014 to 2020, big tech was where you wanted your investments to be.

Last year, though, things started to change… and it’s continued into this year.

IF inflation is here to stay and IF technology will be impacted by the end of quantitative easing and higher interest rates, then our client investment portfolios will be well-prepared for this market shift and any downturn the tech sector might experience… because our clients’ investments aren’t too highly correlated with their career.

Recommendation to solve this problem: Dimensional Fund Advisors

Because tech stocks tend to be so large cap and growth-focused, we like to recommend Dimensional Fund Advisors investment products.

They’re different than tech, and we often use separately managed accounts, which are like creating your own ETF. So, rather than buying shares in an ETF that then invests in 1,500 other stocks, we can take $500,000 or more, and simply buy shares of all 1,500 stocks.

With this, you can make investment decisions at the individual stock level, instead of the all-or-nothing approach we get with ETFs. (We do use ETFs though, especially since separately managed accounts aren’t available for every asset class we want our clients to invest in. They also tend to have lower expense ratios and no transaction fees. But just like with separately managed accounts, we can’t cover every asset class with ETFs, so we use mutual funds to fill in the gaps that exist where ETFs and SMAs aren’t available.)

One of the reasons we like Dimensional Fund Advisors (DFA) so much, is because they focus on dimensions of expected returns. This matters to founders, because when we look at the stock market through history, we can see that the historic average is around 10.3%. (The S&P 500 since 1926.)

But that’s just the average… which we all know is made up of both higher and lower-than-average returns.

DFA targets areas, or dimensions of the market, that produce higher-than-expected returns.

Throughout history, there have been areas of the market that perform above the 10.3% average, including the two specific areas of first value stocks (11.8% on the Russell 1000 Value Index since 1979), and small cap stocks (11.9% on the US Small Cap Index since 1928).

I know 1.5% or 1.6% might not seem like much of a difference at first, but here’s some math for you:

- $1 invested in the S&P 500 in 1926 became $10,937 by 2021.

- $1 invested in the DFA Small Cap Value Index in 1928 (two years later) became $92,668 by 2021.

An 8.5x return difference, just by seeking out and investing in a dimension of the stock market that returns 1.6% higher than average.

Pretty impressive, no?

(Now you can see why we’re such fans of DFA, can’t you?)

Balance your investment portfolio as a tech founder

First and foremost, before you’re a tech founder, you’re a human being desiring financial security. This is what we’re here to help you create, and why we want to help you make sure you don’t tip the weights of your investment portfolio too heavily with tech-only investments.

Putting all your eggs in one basket gives you too much of a “heads you win, tails you lose” kind of scenario, and we’d hate to see the market flip a tails coin on you.

But when you take the time to plan and make an investment strategy (and resulting portfolio) that is diverse enough to be antifragile, it’ll hold up you and your family’s financial future throughout all kinds of different potential future outcomes.

Book a call today to talk to myself or another expert on our team about balancing your investment portfolio, making it antifragile, and putting your investment dollars into the dimensions of the stock market that will give you higher-than-average returns.